Well, if you haven’t already heard, the auto industry closed out 2024 like a well-tuned engine: humming along but with a few hiccups in the gearbox. As we discussed before, November numbers showed a respectable 5.8% year-over-year (YoY) increase in U.S. light vehicle sales, hitting a seasonally adjusted annual rate (SAAR) of 16.5 million units. December, however, kept us on the edge of our seats—waiting for those final figures that scream holiday frenzy.

Looking forward, analysts project sales zooming toward 18 million units by 2028, fueled by pent-up demand (thanks, supply chain issues!) and the revival of fleet and mass-market vehicle sales. The hottest wheels? Crossovers (CUVs) and small pickups. Meanwhile, sedans continue their slow march into irrelevance, much like Blockbuster in the Netflix era. Whoops!

Big winners in the revenue race include Tesla, GM, and Ferrari, proving that innovation, self-driving tech, and luxury vibes are still in vogue. Over in Dearborn, though, Ford’s rising warranty costs and cautious 2025 outlook are causing some nervous revs.

Let’s dive into this month’s econ watch in the automotive industry.

KEYPOINTS:

- The auto industry is rebounding, with stronger inventories, easing loan rates, and rising consumer confidence fueling growth.

- Tesla leads the EV market with strong sales and cutting-edge technology, but legacy automakers like GM and Ford are catching up fast with aggressive electrification strategies. Meanwhile, startups like Rivian and Lucid face profitability struggles despite ramping up production.

- Potential policy shifts under a Trump administration, such as relaxed emissions standards and targeted tariffs, could benefit legacy automakers while creating hurdles for EV startups.

- At the same time, evolving consumer expectations around pricing, financing, and trade-ins remain critical to sustaining demand in 2025.

Inventory & Pricing: High Gear Recovery

As of November, U.S. auto inventory hit 2.97 million units, a welcome comeback after years of slim pickings. Leading the charge? Japanese and Korean automakers, leaving Detroit’s Big Three to play catch-up.

But let’s talk prices—because they’re definitely not stalling. The average transaction price (ATP) for new vehicles revved up 1.5% YoY to $48,724, with SUVs and trucks (the auto industry’s golden geese) leading the pack. Incentives jumped a whopping 53% YoY, but don’t pop the champagne just yet—they’re still stuck below pre-pandemic levels. And used cars? Their prices climbed 11.3% YoY, proving yesterday’s treasures are still hot commodities.

Speaking of budgets, here’s a number to chew on: In Q4 2024, a record 18.9% of new-car buyers signed up for monthly payments over $1,000, according to Edmunds. That’s right—four digits, every month. The average amount financed for new cars also hit an all-time high of $42,113. But here’s the silver lining: most of these buyers are prime borrowers, meaning we’re less likely to see a wave of delinquencies. The used car market, with its heavier subprime mix, can’t say the same.

Now, for the good news: auto loan rates are finally easing up! The average APR for new cars dropped to 6.8% in Q4, down from 7.1% in Q3 and 7.4% last year. Used car APRs followed suit, dipping to 11% from 11.3% in Q3 and 11.6%a year ago.

So, what’s the takeaway? While car buying still feels like splurging on a luxury vacation (every month), falling interest rates and better inventory are steering the market toward smoother roads. Now let’s see if the industry can keep the momentum without running consumers’ wallets off the road!

Couldn’t have said it better ourselves!

The auto market seems to be walking a tightrope between progress and pressure. On one hand, inventories are up, interest rates are finally easing, and buyers are finding more options on the lot. On the other hand, soaring car prices and record-breaking monthly payments are testing just how much consumers are willing—or able—to spend. As we roll into 2025, the question becomes whether falling interest rates can offset sky-high financing amounts. Will buyers keep splurging on their dream SUVs and trucks, or will sticker shock eventually hit the brakes? For now, it’s a mixed bag—some smooth roads ahead, but don’t be surprised if a few potholes emerge along the way.

EVs and Future Themes: Tesla’s Lightning Run

Now, if Tesla were a person, they’d be the one effortlessly acing all the tests. Tesla remains the undisputed EV leader, with strong sales and headline-grabbing tech like full self-driving features. But watch your mirrors, Tesla, because GM and Ford are hot on your tail with electrification strategies like GM’s Ultium platform.

Meanwhile, startups like Rivian and Lucid are trying to keep their heads above water. Production? Rampant. Profits? Not so much.

So, what do we think of the EV industry going into 2025? Looking ahead, here’s what’s charging up the EV world:

- Tightening emissions regulations could drive hybrid and EV sales.

- Autonomous tech and connected cars continue to reshape what “driving” even means.

- Supply chain woes (batteries, chips) will keep automakers on their toes.

Of course, with all the competition, the EV industry feels like a high-stakes Formula 1 race. Tesla’s still leading the pack, effortlessly lapping the competition with sleek tech and record sales, but the pit crew at GM and Ford is working overtime to close the gap. Meanwhile, Rivian and Lucid are like the scrappy underdogs—fighting to stay in the game, even if their profit engines are sputtering. The road ahead promises twists and turns: tightening emissions rules could supercharge EV adoption, while autonomous tech continues to redefine what it even means to "drive." But let’s not forget the challenges—batteries, chips, and supply chain headaches that keep everyone guessing. In this race, the winners won’t just be the fastest; they’ll be the smartest at navigating these challenges. One thing’s for sure—2025’s EV landscape is shaping up to be electrifying. Let’s hope no one runs out of charge before the finish line, literally!

Donald Trump Takes the Wheel: Policies & Predictions

As we talk about EVs, of course Trump’s return to the political fast lane could reshape the auto industry’s roadmap. Expect a rollback of emissions standards and fuel economy rules—music to the ears of legacy automakers like Ford and GM, which churn out profitable gas-guzzling trucks. EV makers like Rivian? Not so thrilled.

On trade, Trump’s tariff rhetoric is revving up. Stricter tariffs could target Chinese imports, nudging manufacturing back stateside. However, Mexico may escape the worst to avoid major disruptions.

Winners:

- Ford and GM, with fewer compliance headaches for their gas-powered behemoths.

- U.S.-based suppliers like Gentex, which sidestep tariff-related cost surges.

- Dealers, who might see a demand bump thanks to relaxed regulations.

Challenged:

- EV startups like Lucid, which rely on stricter environmental policies to nudge buyers into electric cars.

- Suppliers like Aptiv and BorgWarner, who could face a rougher road due to slower EV adoption.

The Trump administration's potential policy shifts signal a rollback to familiar territory for traditional automakers, but this isn’t a free ride to profitability. While relaxed environmental regulations and targeted tariffs might seem like a win for legacy players like Ford and GM, the road ahead is still bumpy. EV adoption is no longer just about regulations—it’s about consumer demand, global competition, and innovation. For startups like Rivian and Lucid, the challenge isn’t just policy; it’s scaling production and finding a foothold in a market increasingly dominated by giants like Tesla. Meanwhile, suppliers caught between geopolitical shifts and the slow pace of electrification must tread carefully to stay competitive. In this environment, adaptability is the key. Automakers who can balance the short-term gains from regulatory relief with long-term investments in innovation and sustainability will be the ones driving the industry forward. And for everyone else? Well, the warning lights are already blinking.

Gearing Up for 2025

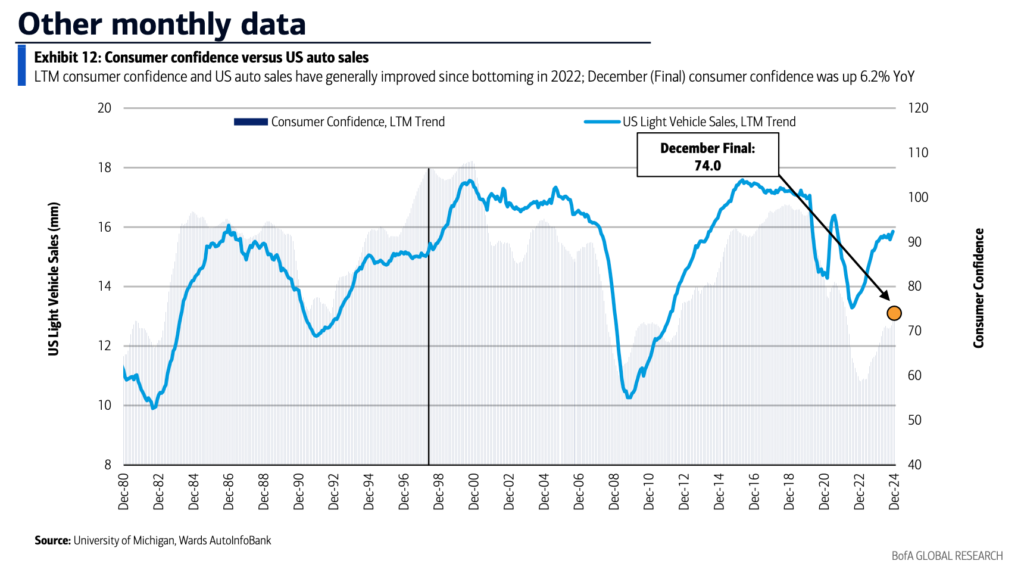

The macro front offered some good news: Consumer confidence rebounded 6.2% YoY in December, and total miles driven in the U.S. hit pre-pandemic levels. Gasoline prices stabilized at $3.13 per gallon, keeping wallets a bit happier and fueling demand for bigger vehicles.

To end the year, car buyers kept their cool — mostly. According to CDK Global, a solid 88% of consumers rated the car-buying process as easy. Sure, that’s a tick down from November’s 91%, but hey, we’re still in “historically high” territory. So, what’s behind this slight dip in buyer bliss?

Where It Got Sticky

- Price Negotiations: Only 61% of buyers left the dealership smiling about the haggling process. It seems getting a “good deal” these days feels more like spotting a unicorn.

- Trade-Ins: Negotiating trade-in values? Let’s just say it’s not winning any popularity contests, with fewer than 52% of buyers giving it a thumbs up.

- Financing: Even the credit application process tripped up some buyers, as satisfaction with financing dropped from 63% in November to 61% in December. Waiting for approval can test even the most patient among us.

The Silver Lining

- Faster Transactions: Speed was the name of the game, with a 20% jump in satisfaction for transaction times. Who doesn’t love a quick pit stop instead of a dealership marathon?

- More Cars, Less Hassle: Over 50% of buyers found their dream car in stock on the first try. Stronger inventories mean fewer compromises — and less settling for “meh” colors like beige.

While having more cars to choose from is a definite win, the real MVP is how smooth the buying experience feels. If dealerships want to keep buyers coming back for more, they might want to turn down the stress on pricing, trade-ins, and financing. Because let’s face it, no one wants to feel like they’re starring in a never-ending negotiation drama.

The car-buying experience in December showed us one thing: consumers want it all—speed, options, and a deal that doesn’t make them cringe. While faster transactions and better inventories are helping dealerships win points, the stumbling blocks of price haggling and trade-in negotiations are still raining on the parade. The lesson here? Shiny cars may draw buyers in, but it’s the experience that keeps them coming back. Dealerships that can fine-tune the art of making customers feel valued, not nickel-and-dimed, will race ahead. For now, car buyers are holding steady—but let’s see if the industry can keep them cruising happily into the new year.

Final Lap: What to Watch

The auto industry is charging into 2025 with momentum and plenty of twists ahead. Recovery is in full swing, fueled by stronger inventories, easing loan rates, and rising consumer confidence. But it’s not all smooth roads ahead—rising costs, geopolitical headwinds, and the evolving demands of the EV race mean automakers will need more than horsepower to stay ahead.

Tesla may be leading the EV charge, but the competition isn’t far behind, with legacy automakers revving up their electrification strategies. Meanwhile, startups like Rivian and Lucid are pushing to carve out their place, even as profitability remains elusive. And then there’s the wildcard of policy changes under a Trump administration—will they turbocharge traditional automakers or throw a wrench in the gears of EV progress?

In short, the industry isn’t just recovering; it’s transforming. From tightening emissions rules to autonomous tech breakthroughs, automakers must juggle innovation, affordability, and shifting consumer expectations. So buckle up—2025 promises to be a ride worth watching. Whether it’s smooth cruising or sharp turns ahead, one thing’s for sure: the auto industry never idles.