KEYPOINTS:

- GM and Ford are in a better position than Stellantis due to their diversified business models, which include credit services, and generally newer product lineups that appeal more to consumers.

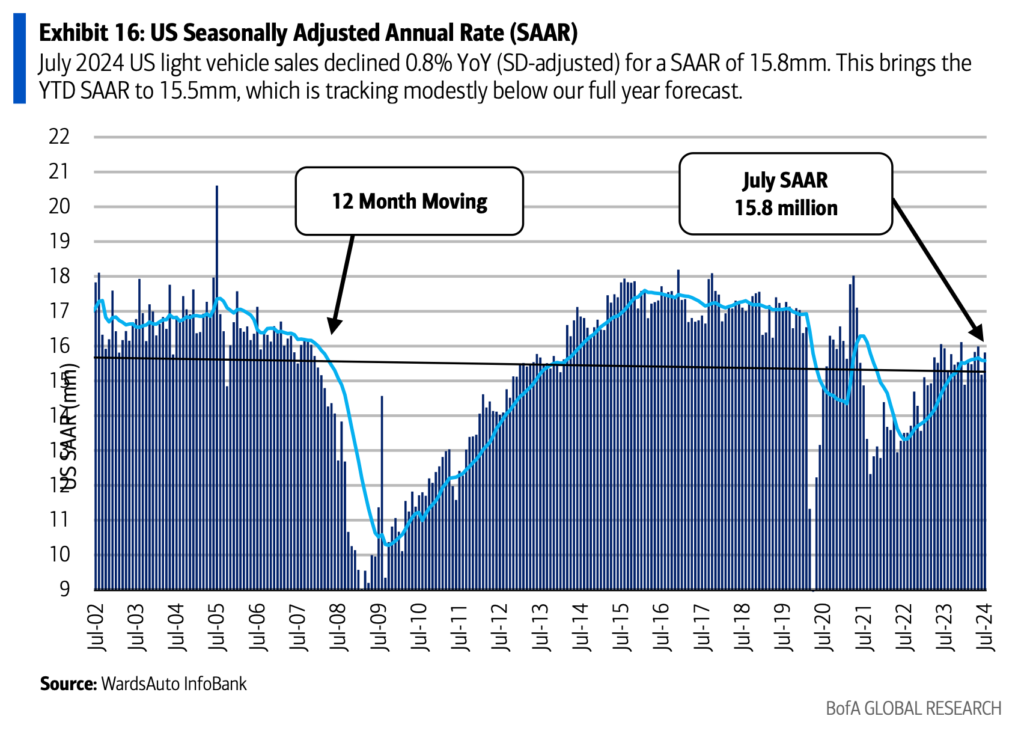

- The automotive industry is experiencing high inventory levels, which may lead to further production cuts despite plans to increase production in the fourth quarter.

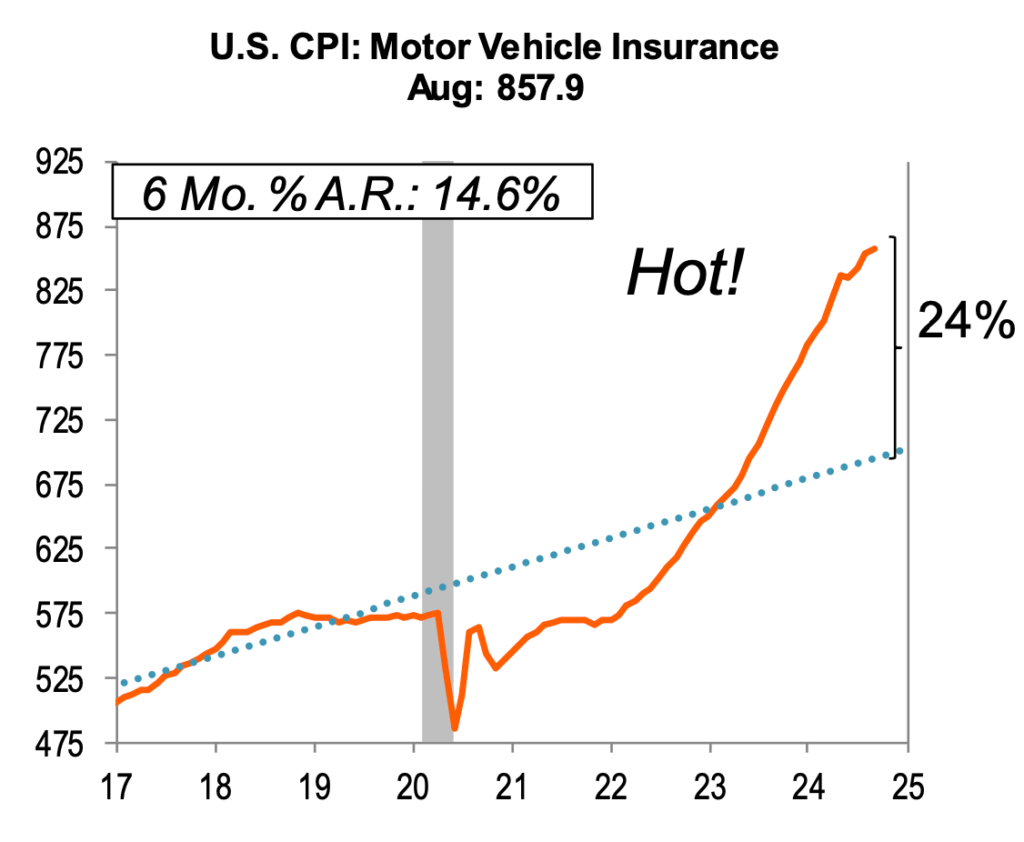

- A significant increase in auto insurance costs over the years has boosted revenues for insurance companies but has made owning and insuring vehicles more expensive for consumers, contributing to a decline in vehicle sales. This trend is expected to continue until there is some economic relief.

- Real consumer spending on new motor vehicles has been volatile, with significant drops and slight recoveries reflecting consumer hesitance and potential financial strain.

Struggle of Stellantis

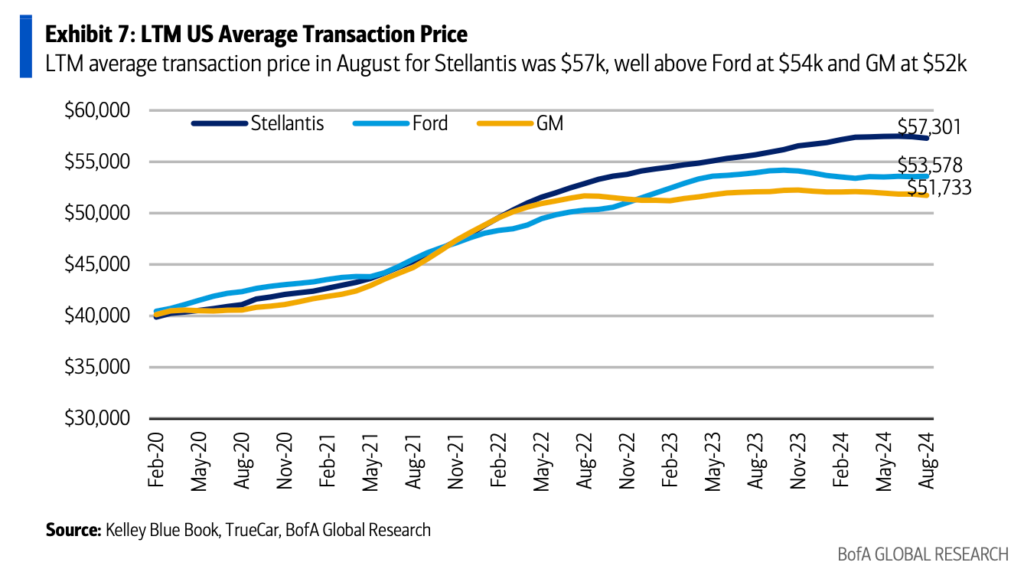

Stellantis is hitting a rough patch, adjusting its profit forecasts downward amidst escalating costs and market challenges, particularly in key regions like North America and China. The company’s woes are exacerbated by hefty incentives on aging vehicle models and bloated inventories that are eroding profit margins and straining cash flows. In contrast, rivals GM and Ford seem to be cruising on smoother roads, thanks to their diversified ventures into financial services which bolster their income streams and buffer against similar market pressures.

Unlike its competitors, Stellantis is grappling with a product lineup that’s getting long in the tooth; its average vehicle replacement rate for the model years 2025 to 2028 lingers at 18.8%, just shy of the industry norm of 19.4%. This sluggish pace in refreshing its offerings could further dent its market share and profitability, particularly as consumers lean towards newer, more innovative models offered by competitors.

Moreover, Stellantis’s strategy of maintaining higher inventory levels and pricing its vehicles above those of GM and Ford has only complicated its market dynamics, making it harder to balance supply with flagging demand. While GM and Ford have cautiously managed their pricing and inventory, steering clear of aggressive stockpiling in recent years, they are positioned more robustly against market fluctuations.

The financial vitality of legacy automotive manufacturers like GM and Ford is further evidenced by their robust financial results, attributed largely to their ability to command premium prices for their vehicles. However, not all is smooth driving; Ford, for instance, is navigating costly turbulence due to a spike in warranty claims, impacting its bottom line.

Stellantis faces a more daunting road ahead, particularly in North America where its older vehicle lineup and high operational costs are proving to be significant hurdles. With industry forecasts suggesting a gradual uptick in sales peaking by 2028, fueled by pent-up post-pandemic demand and increased fleet sales, there’s a glimmer of hope if strategic adjustments can be made swiftly.

Suppliers in the automotive sector are also feeling the pinch, with a polarized financial performance landscape. Some have thrived on shrewd management and operational efficiencies, while others falter, hampered by reduced production volumes. This has led to a recalibration of financial forecasts across the supplier spectrum, underscoring the industry’s volatile nature.

? In a nutshell, while Stellantis struggles to navigate current market headwinds with an outdated fleet and squeezed margins, GM and Ford appear to be steering a more favorable course, armed with diversified revenue streams and fresher product offerings. The road ahead for Stellantis will require nimble adjustments and perhaps a sharper focus on innovation and market repositioning to regain its competitive edge.

What’s Going On in the EV Market?

The electric vehicle (EV) market was supposed to be zipping along the fast lane by now, but instead, it’s taking a bit of a detour. Growth hasn’t hit the high speeds expected, leading to production delays and missed financial targets. Despite these bumps in the road, companies like Tesla are playing a clever game of financial keep-away, thanks to regulatory credits. These government incentives, designed to encourage EV manufacturing, are helping to cushion the financial potholes caused by slower sales.

Lucid Motors, another player in the EV scene, is also making some noteworthy financial maneuvers. With fresh financing from optimistic investors, Lucid is gearing up for future projects that could electrify its market presence. This financial backing is crucial, especially when the broader automotive sector is hitting a few speed bumps. The downturn in global automotive production forecasts for 2024 has thrown a wrench in the works for suppliers, who are facing reduced demand for their components and materials. This chain reaction is forcing many suppliers to dial back their financial expectations for the year, marking a tough chapter in the automotive narrative.

? While the EV sector might not be accelerating as quickly as once hoped, strategic financial plays and a bit of regulatory support are keeping key industry players like Tesla and Lucid Motors in the race.

Auto Insurance Boosting Overall CPI.

The steep climb in auto insurance costs has proven to be a double-edged sword. While insurers are seeing their revenues shift into high gear, the burden on consumers has pumped the brakes on new vehicle purchases. The fallout from the COVID-19 pandemic initially saw a spike in vehicle sales, but the persistently high costs of cars and insurance have since made ownership less palatable for the average consumer. As a result, the sales momentum has sputtered, with fewer consumers willing to shoulder the added financial load.

In this challenging economic climate, the sticker shock isn’t just confined to the auto industry. Consumers are tightening their belts all around, especially when it comes to non-essential goods. The high costs associated with maintaining a vehicle are causing a ripple effect, where discretionary spending takes a nosedive. This cautious approach to spending is likely to continue rumbling through the market until a significant economic upswing or a boost in consumer confidence can reignite the willingness to spend. Until then, the road to recovery for car sales looks to be a bumpy ride, with potential buyers waiting for a clearer, more financially favorable horizon.

? As the gears of the economy grind slowly, the automotive industry faces a peculiar challenge: to navigate through the murky waters of high operational costs and cautious consumer spending. If the trends hold, it might be a while before we see a significant uptick in vehicle sales. However, any reduction in auto insurance costs or an overall economic improvement could be the jumpstart needed for consumers to rekindle their interest in new cars. Until then, it's a waiting game to see how long it takes for consumer confidence to rev back up to its former glory.

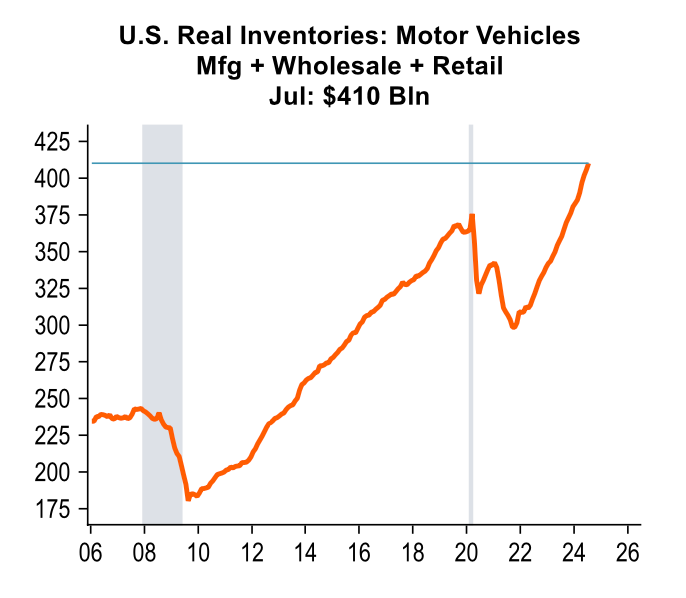

Inventory Mismatch? What’s Happening?

The auto industry finds itself in a curious predicament as it navigates the choppy waters of a market that isn’t quite ready to bounce back. Even as production cutbacks were seen in the third quarter, manufacturers are paradoxically gearing up to slightly increase output in the fourth quarter. This optimistic gamble amidst stagnant sales may sound like a plot twist in an economic thriller—where demand doesn’t quite catch up to supply, leaving lots filled with unsold cars. Indeed, the mismatch between the cars rolling off the production lines and the actual sales could lead to an ever-growing inventory, potentially necessitating yet more cuts if these vehicles continue to gather dust.

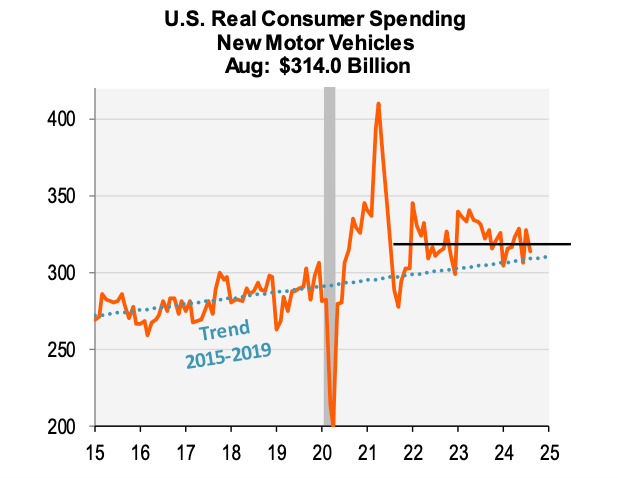

Real numbers paint a stark picture: while nominal consumer spending on new motor vehicles was reported at a robust $378.2 billion in August, the real consumer spending, when adjusted for inflation, tells a different story at just $314.0 billion. This gap underscores how inflation is eroding purchasing power, putting a further damper on an already subdued market. So, while auto companies might be revving up production in hopes of a sales rebound, the reality on the ground suggests they might have to pump the brakes unless consumer confidence—and spending—picks up speed.

? As we witness the automotive industry's strategic maneuvers, it's clear they're playing a high-stakes game of expectation versus reality. With inventories brimming and consumer wallets tightening under inflationary pressures, the road ahead looks uncertain. Will the industry's optimistic production increase in the fourth quarter lead to a sales resurgence, or will it add to the growing pile of challenges? Only time will tell, but one thing is certain: the balance between production and market demand will be crucial in steering the future course of the auto sector. For now, it's a waiting game, with the industry's pulse closely tied to economic signals and consumer sentiment.

Consumer Spending on Vehicles

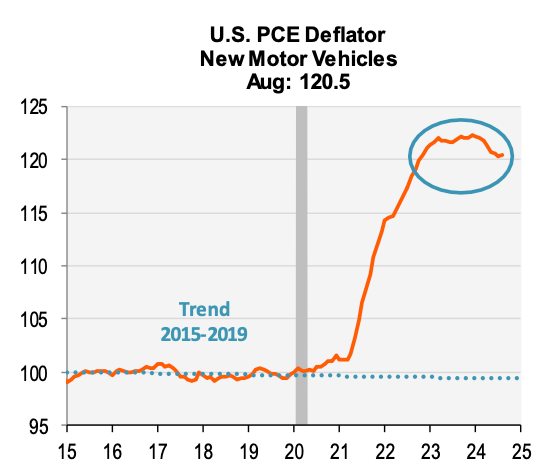

In August, the PCE deflator for new motor vehicles hit a notable 120.5, a stark increase from the base index of 100. This jump signals a significant inflation spike within the auto sector, underlining just how much more expensive new vehicles have become over the base year. The surge in prices isn’t just a number on a page; it translates into steeper costs at the dealership, putting new cars out of reach for many average buyers. As vehicle affordability shifts into the slow lane, consumer demand is hitting the brakes, which could lead to a slowdown in auto sales. This financial squeeze is reshaping the automotive market landscape, where the cost of getting behind the wheel is accelerating faster than many wallets can keep up.

Real consumer spending on new motor vehicles has been on a roller coaster, showing stark fluctuations that mirror consumer uncertainty and economic pressure. Notably, spending took a nosedive by 5.4% in the last quarter of 2023, only to rebound with a 4.7% increase at the start of 2024. This was followed by a negligible dip of 0.1% in the second quarter, and then a more pronounced drop of 4.4% in the third quarter.

However, the market seems to be correcting itself slightly, with a modest 1.2% uptick anticipated in the fourth quarter. These swings in spending reflect not just the volatility in consumer confidence but also highlight the broader economic climate, marred by rising inflation and job market jitters. As belts tighten, the discretionary splurge on new vehicles remains subdued, hinting at ongoing financial caution among buyers, making it a bumpy ride for automakers trying to steer through these unpredictable economic currents.

? This ebb and flow in automotive spending showcases a broader narrative of consumer behavior: when economic signals flash red, wallets snap shut, but a glimmer of recovery can quickly loosen the purse strings. Automotive companies, therefore, need to stay nimble, aligning their strategies closely with these economic pulse points to anticipate shifts and adapt swiftly. The road ahead may be uncertain, but by understanding these patterns, the industry might better navigate the turns and tune their engines accordingly.

Conclusion

In conclusion, the American automotive industry finds itself at a critical crossroads. Currently, it grapples with several significant challenges: reduced consumer spending power, mismatched production and sales, and alarmingly high inventory levels. These issues are not just fleeting concerns but are indicative of deeper systemic shifts within the economic and consumer landscapes. The prolonged mismatch between production outputs and actual sales has led to burgeoning inventories, signaling a potential oversupply in the face of waning demand. This situation is exacerbated by the fact that the cost of vehicles continues to climb—a direct result of inflationary pressures that further dampen consumer purchasing power.

Ultimately, the path forward for the American automotive industry will require a blend of strategic foresight, innovative thinking, and an unwavering commitment to adapting to the fast-changing economic environment. With thoughtful adjustments and a keen focus on market demand, the industry can steer itself back to a course of sustained growth and profitability.