The automotive industry has demonstrated remarkable resilience and adaptability, navigating a complex landscape shaped by the post-pandemic recovery and ongoing economic fluctuations, proving to be a master of comebacks! As we move through the first half 2024, key indicators such as consumer confidence, vehicle sales, inventory levels, and the shift towards electric and hybrid vehicles provide critical insights into the industry’s current state and future direction.

KEYPOINTS:

- Consumer confidence remains strong and healthy

- People are still buying cars despite lots of macroeconomic pressures

- Inventory is good, but used cars supply is scarce

- Issue of high EV prices needs to be addressed soon, says Stellantis CEO

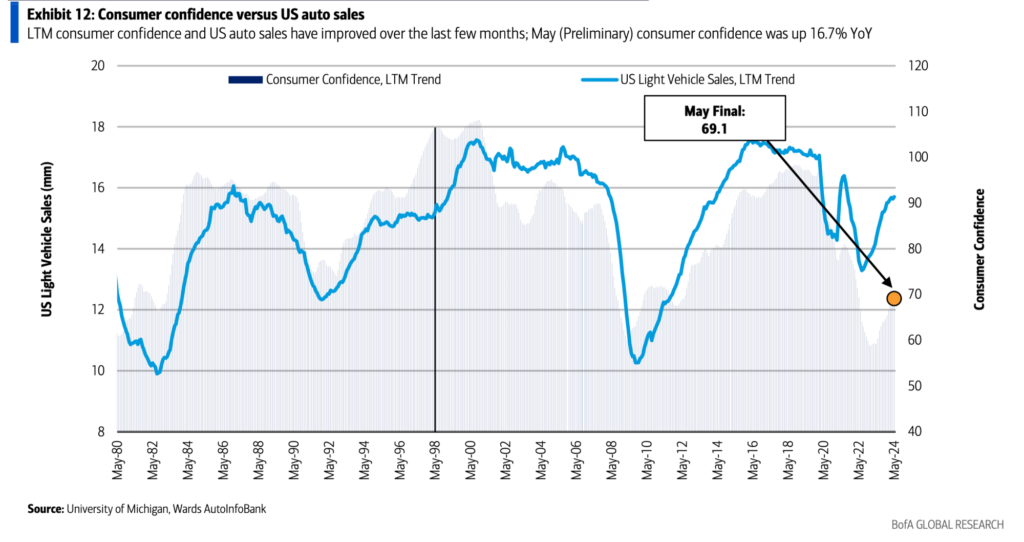

Consumer Confidence Going Steady

Ladies and gentlemen, hold onto your hats, because consumer confidence is soaring like never before, driven by employment rates that are loud and proud, leading to higher disposable incomes. When people have the money, what would they do? Splurge on that fancy new ride, of course. People are feeling so good about their wallets, they’re practically throwing money at car dealerships.

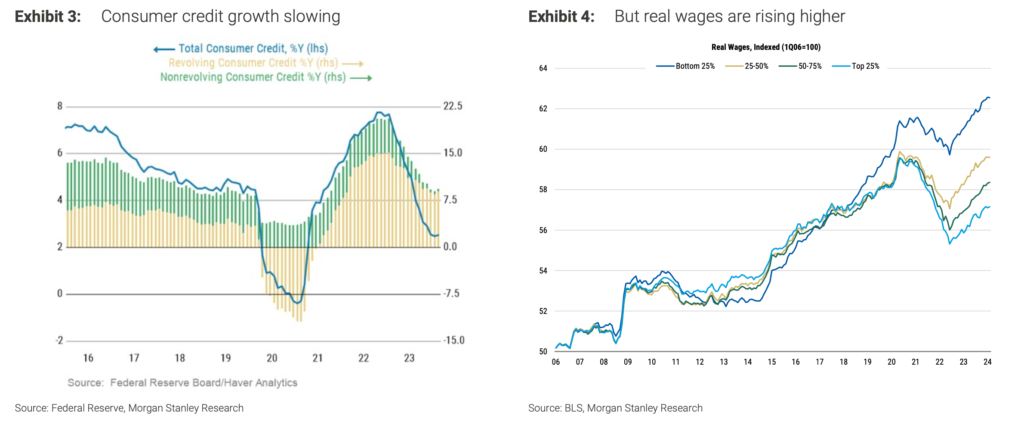

Sure, it looks like consumer credit growth is slowing, but considering the growing SAAR in May, it only means that there is a targeted borrowing. Consumers might not be on to shopping for disposable items like clothes and the likes, but more on to the bigger deals. Really, look at them go.

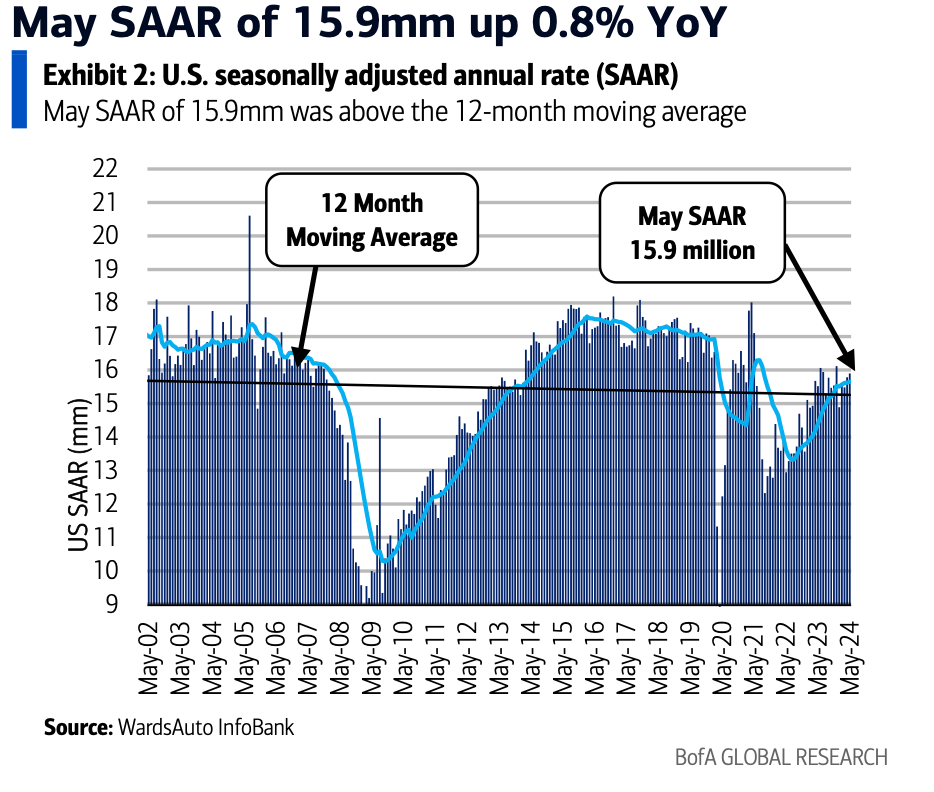

With an SAAR of 15.9 million vehicles, May 2024 brought us a mild, but delightful surprise compared to April’s SAAR of 15.8 million vehicles, its a highlighting growth in trend that could make even the most pessimistic economist crack a smile.

? BMW, Tesla, VW, Ford, and Honda are riding high on this wave, thanks to their stellar market strategies and product offerings. Meanwhile, GM and Nissan are lagging behind, perhaps spending too much time napping instead of innovating. Tut tut, looks like innovation is everything these days. If you’ve got nothing new, then you’re out of the game.

Production Constraints and Inventory Status

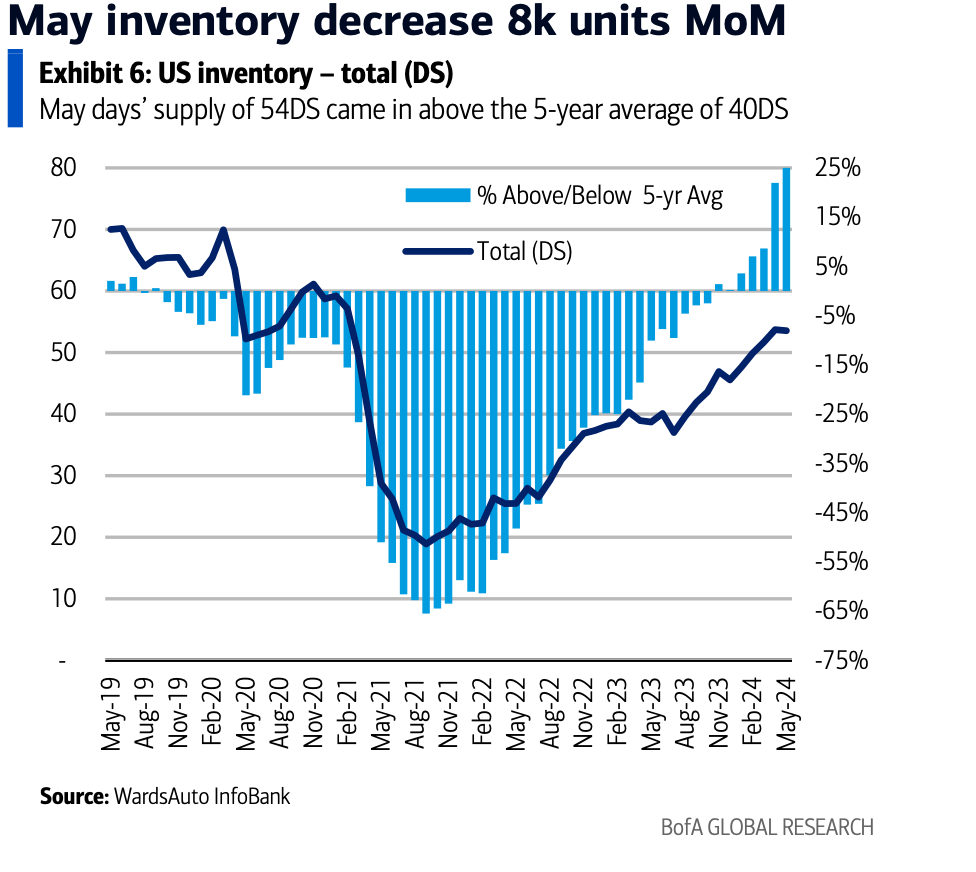

Now, onto inventory levels. We’ve got a stable 2.7 million units at the end of May, unchanged from April. This steady climb over the past two years placed us in the “normal” range of 2.5 to 3.0 million units. It’s like walking a tightrope—keeping prices steady while suppliers grumble about wanting more volume.

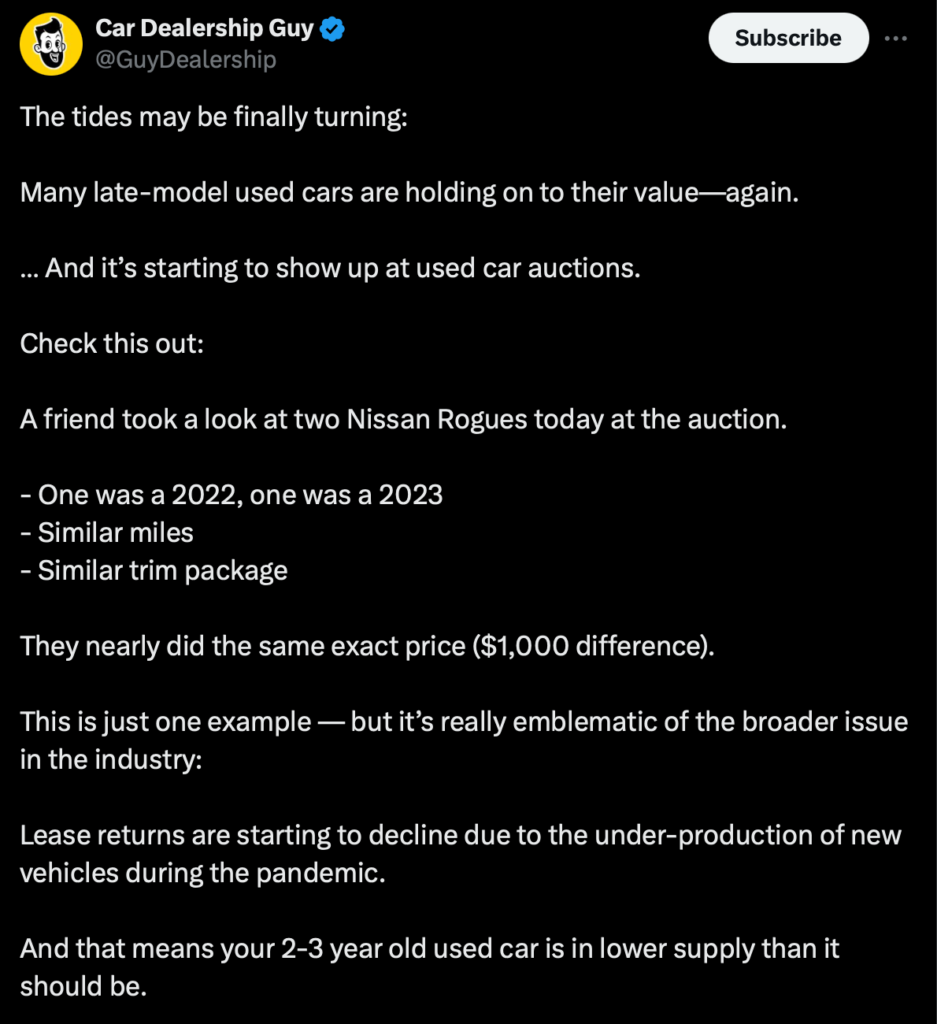

Also, the supply of used vehicles aged 0-6 years is shrinking extremely fast, and it’s expected to keep dwindling through 2025. Used car dealers are pulling their hair out trying to find late-model vehicles, which are more sought after than ever. It’s a problem that’s not going away anytime soon, and would be a pain in the rear end for used car dealerships. The scarcity of these vehicles, which are typically more in demand, underscores the ongoing tension between inventory levels and market demand.

? Keep up, Stellantis, we’re rooting for you! Because cheaper parts, meaning cheaper cars, and its a high five for middle class consumers.

The New Race to Cutting EV Prices

Cut it out, says Stellantis CEO, Carlos Tavares, the man with a plan, has put a tight squeeze on suppliers to cut the costs of EV components and speed up their game. The current high costs and turtle-like pace of production are making some companies, namely Stellantis consider insourcing—because if you want something done right (and cheaper), well be damned, you’ve got to do it yourself.

That means automakers like Stellantis are “not in a race to transition to EVs, but in a race to cut costs on EVs” as they seek to build battery-powered cars that are affordable for the middle class.

The EV race has become a cost-cutting race, and it will be a “big, big, big burden” on parts suppliers, Tavares said, considering the vast majority of any new vehicle’s production costs come from its parts.

You can already see in Europe, significant tier-one suppliers with very well-known names that are already in trouble for this specific reason.

Carlos Tavares

Traditional automakers, again, namely Stellantis are feeling the heat from Tesla and other EV start-ups, who have mastered the art of low-cost, efficient production. It’s a dog-eat-dog world out there, and everyone’s trying to stay in the game.

? Keep up, Stellantis, we’re rooting for you! Because cheaper parts, meaning cheaper cars, and its a high five for middle class consumers.

- GM: GM is playing the long game, betting big on the future of EVs. They’ve got optimism in spades and are making strategic moves to stay ahead.

- Ford: Ford’s got a diversified strategy, offering various powertrains to keep everyone happy. It’s like a buffet of automotive options.

- Tesla: Tesla’s got its hands in all the cookie jars, from Full Self-Driving (FSD) to Robotaxis, all while trying to keep up with EV demand. It’s a juggling act worthy of the circus.

Despite all the EV hype, automakers are pumping the brakes and reconsidering their rapid shift. Instead, they’re extending the life of internal combustion engine (ICE) programs and dabbling in hybrids—though let’s be honest, it’s more talk than action at this point. The market’s as uncertain as a coin toss, and everyone’s leaning on their trusty gasoline and diesel sales to fund future endeavors.

Automakers need to balance ICE, hybrid, and EV production, while keeping an eye on consumer preferences and regulatory changes. So it will be a critical and tough next few years, and it’s going to be one hell of a rollercoaster ride with a lot of uncertainty and volatility. It’s a delicate dance of strategic planning and flexibility, especially for automakers.

Outlook for the Next Month

The automotive industry is in a state of flux, showcasing remarkable resilience and adaptability amid rising consumer confidence, increasing vehicle sales, stable inventory levels, and a complex shift towards EVs and hybrids. This landscape is a testament to the industry’s ability to navigate post-pandemic recovery and ongoing economic fluctuations.

To thrive in this unpredictable environment, automakers must stay agile, balancing the production of internal combustion engine vehicles with the rising demand for electric and hybrid models. They need to keep a keen eye on consumer preferences, regulatory changes, and the ever-evolving market dynamics. The ability to pivot strategically and efficiently will be crucial.

As we move forward, the industry’s success will depend on its capacity to innovate, reduce costs, and meet the diverse needs of consumers. It’s a delicate dance of strategic planning and flexibility, ensuring they remain competitive in a rapidly changing market.

The next few months will be critical in shaping the future direction of the automotive sector. Stakeholders must remain vigilant, ready to adapt to new challenges and opportunities that arise in this dynamic landscape. Guess we’ll just have to see how it goes.